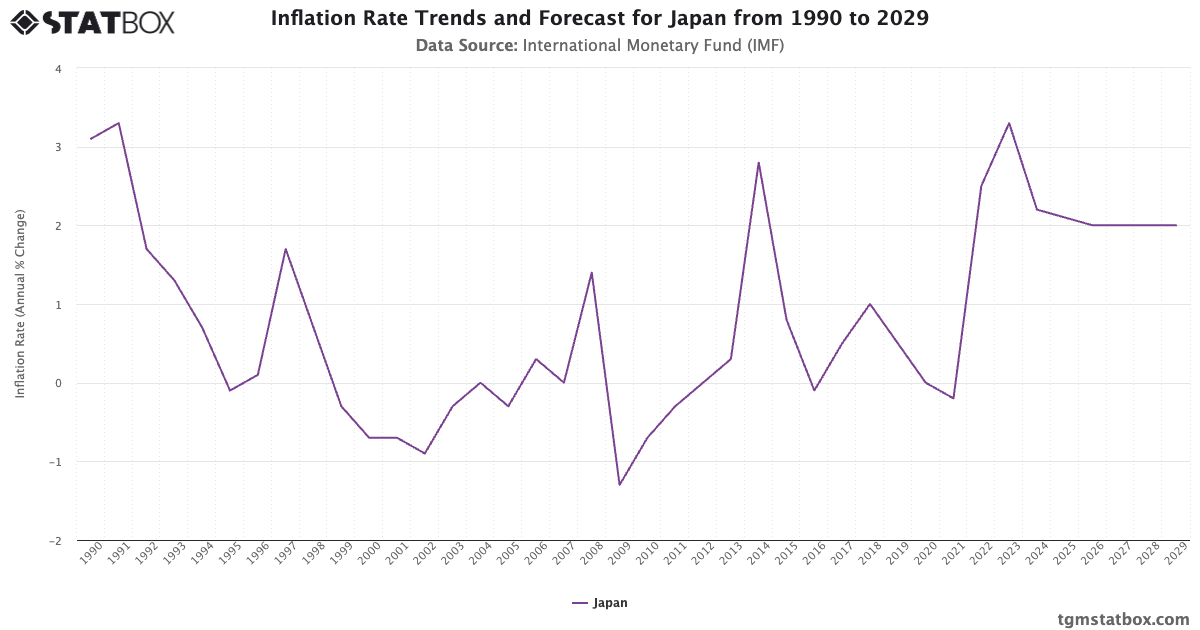

Japan’s latest inflation data suggests a cooling trend that masks a much more volatile reality. While the headline Consumer Price Index (CPI) slowed for a fourth consecutive month in February and core inflation narrowly missed market estimates, the numbers do not tell the story of a victory over rising prices. Instead, they reveal a central bank caught between a weakening currency and a domestic economy that refuses to follow the traditional rules of global finance. The Bank of Japan (BoJ) is currently attempting to navigate a "soft landing" out of negative interest rates, but the cooling data might actually be a sign that the window for a clean exit is slamming shut.

The February data showed core CPI—which excludes fresh food—rising 2.8%. On paper, this looks like a retreat from the highs of the previous year. To the casual observer, it appears the "inflation monster" is being tamed. It isn't.

The Statistical Mirage of Cooling Prices

A significant portion of the recent "cooling" in Japanese inflation is not the result of organic market stability or improved supply chains. It is the result of aggressive government intervention. The Japanese administration has been pouring subsidies into utility bills, effectively masking the true cost of energy for the average household. When you strip away these artificial suppressants, the underlying inflationary pressure remains stubbornly high.

Economists often focus on "core-core" inflation, which strips out both fresh food and energy. This metric has remained consistently above the BoJ's 2% target for over a year. The problem for Governor Kazuo Ueda is that the headline number is what drives public perception and, more importantly, wage negotiations. If the headline number continues to "ease" due to government subsidies, labor unions have less leverage to demand the historic pay raises needed to create a self-sustaining economic cycle.

Japan is currently trapped in a circular logic. The BoJ wants "virtuous" inflation driven by demand and wages. However, the inflation Japan actually has is "cost-push" inflation, driven by the expensive import of raw materials. Because Japan imports almost all of its energy and a massive portion of its food, the price of these goods is tied directly to the value of the Yen.

The Yen Problem Nobody Wants to Solve

The Japanese Yen has been on a downward spiral against the US Dollar for the better part of two years. This is not an accident; it is the direct consequence of the interest rate gap between the BoJ and the Federal Reserve. While the rest of the world hiked rates to fight post-pandemic inflation, Japan kept its rates at the bottom of the ocean.

This policy has turned the Yen into the world’s favorite "carry trade" currency. Investors borrow Yen for next to nothing and dump it to buy higher-yielding assets in Dollars or Euros. This constant selling pressure devalues the Yen, which in turn makes every barrel of oil and every bushel of wheat Japan buys more expensive.

The BoJ is essentially subsidizing global investors at the expense of the Japanese consumer’s purchasing power.

We are seeing a breakdown in the traditional relationship between currency and exports. Historically, a weak Yen was a boon for giants like Toyota and Sony because it made their products cheaper abroad. Today, many of these companies have moved production overseas. The "weak Yen benefit" has diminished, while the "weak Yen penalty" on energy and food imports has grown. The February inflation miss isn't a sign of health; it’s a sign that the Japanese consumer is finally tapping out.

The Ghost of 1990

To understand why the BoJ is so hesitant to move, you have to understand the institutional trauma of the 1990 market crash. For three decades, "deflation" was the boogeyman. The Japanese central bank spent billions trying to spark even a tiny bit of price growth. Now that they finally have it, they are terrified of killing it too soon.

There is a pervasive fear among Japanese policymakers that if they raise interest rates even by a fraction of a percent, the fragile recovery will collapse, and the country will slide back into the "lost decades" of stagnation. This leads to a policy of "wait and see" that often results in being "too little, too late."

Consider the math of Japan’s national debt. Japan has the highest debt-to-GDP ratio in the developed world.

$$\text{Debt-to-GDP Ratio} = \frac{\text{Total Government Debt}}{\text{Gross Domestic Product}}$$

In Japan’s case, this figure hovers around 250% to 260%. When interest rates are at 0% or negative, servicing this mountain of debt is manageable. But if the BoJ is forced to raise rates to 1% or 2% to defend the Yen or combat runaway inflation, the interest payments alone could consume a terrifying portion of the national budget. The BoJ isn't just managing an economy; it is managing the solvency of the state.

Why the February Miss is Dangerous

The fact that inflation missed estimates in February is being framed by some as a reason for the BoJ to stay the course. This is a dangerous misinterpretation. The miss suggests that domestic demand is weakening. If prices are "easing" because people can no longer afford to buy things, that isn't a healthy economic correction—it's the start of a recession.

Retail sales data shows a trend of "shrinkflation" and "down-trading." Consumers are moving from brand-name goods to store brands, and from fresh meat to processed alternatives. This indicates that the 2.8% inflation rate, while lower than the 3% or 4% seen elsewhere, is still far outstripping the actual wage growth of the average Japanese worker.

If the BoJ waits for "perfect" conditions to normalize policy, those conditions may never arrive. The gap between the US and Japanese economies is widening. If the Federal Reserve keeps rates higher for longer—which current US inflation data suggests it might—the pressure on the Yen will become unbearable.

The Looming Wage Decision

The true "make or break" moment for Japan isn't the CPI data; it’s the annual Shunto wage negotiations. For decades, these negotiations resulted in measly 1% or 2% raises. This year, there is pressure for 5% or more.

If companies agree to these raises, they will inevitably pass the cost on to consumers, leading to another spike in inflation. If they don't, the consumer's spending power will continue to erode, and the economy will stall.

The BoJ is betting that they can thread the needle: get the wage hikes, keep interest rates low enough to support the debt, but high enough to stop the Yen from collapsing. It is a feat of financial gymnastics that has never been successfully performed on this scale.

Institutional Inertia and the Global Context

Japan does not exist in a vacuum. The slowdown in the Chinese economy—Japan’s largest trading partner—adds another layer of complexity. As Chinese demand for Japanese machinery and components drops, the Japanese industrial base loses its primary engine of growth.

This makes the BoJ even more reluctant to tighten policy. They are watching a cooling global economy and a cooling domestic CPI and concluding that the safest move is to do nothing. But "doing nothing" is a choice with its own set of violent consequences. It guarantees the continued debasement of the Yen and the continued "stealth tax" on every citizen who needs to heat their home or buy groceries.

The February inflation data is a symptom of an exhausted economy, not a stabilized one. The Bank of Japan is running out of road, and the "miss" in estimates should be viewed as a warning siren that the temporary window for a controlled exit from ultra-loose monetary policy has likely already passed.

Watch the Yen, not the CPI. If the Yen breaks past the 152 or 155 level against the Dollar, the BoJ will be forced to act regardless of what the inflation data says. At that point, they won't be choosing to normalize; they will be reacting to a crisis.

The strategy of the central bank has moved from "calculated stimulus" to "desperate maintenance." Investors and analysts who view the February cooling as a sign of a returning "normal" are missing the structural rot underneath. The Japanese economy is not cooling down; it is being frozen out by a currency that no longer serves its people.

Demand for Yen-denominated assets is currently driven by speculation rather than fundamental economic strength. This creates a "hollow" economy where the stock market (the Nikkei) can hit record highs while the actual standard of living for the populace declines. This divergence cannot last forever.

The next few months will determine if Japan can actually transform its economic model or if it will remain a cautionary tale of what happens when a central bank waits too long to face reality. Moving interest rates by 0.1% might seem like a small step to the rest of the world, but in Tokyo, it represents the end of an era and the beginning of a very uncertain future.